Financial Plan – A Simple Way to Invite Maa Lakshmi Home

A Small Jump to Leapfrog the Average

A Morning at the Bank: Welcome to Chaos

Earlier this month, I found myself standing in a public sector bank. The counter I was asked to go to had a sizeable crowd pushing for their turn. Two adjacent counters were almost empty.

Naturally, the question popped into my head — why such a lopsided allocation of work, especially during peak hours? But whom should I even ask?

The lady at the crowded corner counter was clearly overwhelmed. The woman at the next counter had barely two people to tend to, but didn’t even return my pleading glance. And the gentleman at the second counter on the right, sunk in a bunch of files, was too far for me to shout across without losing my hard-earned place in the queue. The branch manager’s cabin was even farther, with a mini queue of its own. The busy guard behind me at the branch gate was the unofficial clerk, surely taking some substantial popularity off the plate of the most popular lady in the branch.

“There must be some logic to the system,” I told myself, pacifying my unwillingness to act. Humans can rationalize anything, after all. Can’t they?

I dislike visiting public sector banks for exactly these reasons, but every once in a while, it becomes unavoidable. This time, I was there to help a low-income earner who didn’t meet the relatively high (formal plus invisible) entry barriers of private banks. She needed to open a simple account to start saving a few thousand rupees each month. Despite the crowd, I was inching ahead reasonably well, while occasionally being elbowed by latecomers sneaking in from the sides.

A VIP in the Chaos

At a jammed traffic light, someone will always squeeze in from the edge and overtake you. It’s business as usual. But as I inched ahead patiently to the zebra crossing before the light, the traffic police (lady at the counter) turned off the lights. A VIP is about to pass through the crossing. Damn!

The elderly man in front of me in the queue wanted to open an FD. The lady at the counter suddenly shifted gears. She began convincing him to invest in a mutual fund instead. And just like that, all fatigue disappeared from her face.

Her voice grew calm and confident. The peak hour rush didn’t bother her anymore; it perhaps was never so-peak, after all. Next in line in the queue, I turned invisible to her.

The protagonist in Tushar Kapoor’s Gayab (I know, who remembers that movie🙄) turned invisible upon his own wish; the lady in front of me held similar powers over me and some others around. Additionally, she now had Yudhishthir’s calm with Arjuna’s focus.

Her responses were laser-sharp: “Sir, FD returns won’t be that good.” This remained the backbone of her every answer to the gentleman’s question over the next few minutes. Then came the gentleman’s agreement and a trailing couple of queries, “how much risk do you want to take” and “for how many years” from the lady, the answers to which were “not much” and “3 years”, respectively.

“Great, sir. Large-cap fund it is.”— the deal was done. The loyal guard of the branch took over the deal closure formalities from her.

With that, her attention snapped back to the queue. Tushar Kapoor was visible again. The crowd reappeared around the counter.

A Lot to Be Asked, A Lot Left Unanswered

Some of you who’ve read my earlier musings might recall Tom Sawyer from Whitewashing the Fence — perhaps from my rendition of the tale in the context of the banks, if not from its original author, Mark Twain.

Now, our lady at the counter wasn’t quite a Tom Sawyer — after all, she wasn’t pushing ULIPs or money-back plans with fat commissions. But still, something about that “conversation” made me uneasy.

Think about it: those two quick questions at the end — “How much risk do you want to take?” and “For how long?” — do they really count as risk profiling?

I may say I don’t want to take much risk, but that doesn’t mean I don’t have the ability or even the need to take some. And what did “risk” mean to the senior fellow anyway? Was it market volatility? Losing capital permanently? Or the risk of not having the money handy after three years — the period he mentioned? Was his three-year horizon a necessity or just a preference? We’ll never know, because the questions never reached there.

And the solution? Even more confusing. Why would anyone recommend a 100% equity fund — even if it’s a large-cap one — for just three years? That’s not investing. And what about that confident promise of “low double-digit returns”? On what basis?

The lady should’ve had a lot more to ask — and since she didn’t, she left a lot unanswered. Well, at least in my head.

On the ground, I stayed quiet. I just wanted to get through the queue without losing my patience — or risking the banking access I was trying to gain for the poor woman I’d brought along.

But wait, who am I to be asking all this, even in my head?

An Ex-Banker’s Déjà Vu

I’m an ex–banker myself. I started my career in retail banking back in 2007 — and left it in less than two years. If you’ve read my earlier piece cited above, this may sound familiar, but it bears repeating: it didn’t feel right to build a career on the back of other people’s misplaced trust.

There are many ways to break that trust. One is obvious — selling harmful products knowingly. The subtler one is using a good product the wrong way: recommending it without caring whether the person really needs it.

What if that elder fellow needs to have the money for something non-negotiable after 3 years, and the market is down by 30% at that time? Could be down even by 50%, who knows! Where’s the padding for that contingency, the downside protection, in our trusted banker’s prescription?

Trust comes easily when it comes to banks. Banks make up the largest group among India’s top mutual fund distributors, accounting for nearly 20% of the industry’s regular-plan AUM in FY24-25.

That’s apart from the many other financial products they push — some of which are simply toxic for investors. So, the kind of “due diligence” (or lack of it) we saw at that counter isn’t an exception — it’s the norm. It was the norm when I was a banker; it is the norm today.

But That’s How Averages (Most People) Work

In addition to the bankers, there’s another group that commands massive trust today — the so-called finfluencers.

Sure, there are a few who genuinely educate. But as a group, they also too often have vested interests. They may not directly manage your money, but indirectly, they influence — and often mislead — how you manage it.

But who’s complaining? The music’s still playing — revenue targets are met, commissions and bonuses are earned, jobs are safe. Until, of course, the tide turns.

As Warren Buffett said, “Only when the tide goes out do you discover who’s been swimming naked.”

And that’s exactly where most people go wrong.

Most people realize too late, like those who keep taking antacids for heartburn, only to end up with a heart attack.

Good Planning Spares You a Heart Attack

A good financial plan, like a good workout plan, spares you both the heart attack and perhaps most heartburn too.

I’m often shocked at how easily people hand over their hard-earned money to bankers or “experts” without ever asking for a full, holistic picture.

We very often come across people from across income levels with portfolios that look like puzzles missing half their pieces:

Some are overloaded with gold,

many are over-invested in real estate,

some cluttered with a vast collection of all kinds of mutual funds,

some buried under debt,

some are trapped in high-cost products,

many running on dangerously low liquidity, and

a surprising number are mis-insured or grossly underinsured.

Generally, people who avoid planning face a mix of all these issues. As the saying goes, there’s never just one cockroach in the kitchen. The rot usually runs deep. The financial heart attack is a high probability event for them, bound to happen at some point in time – and even if avoided somehow, the symptoms don’t indicate a thriving, exuberant money life.

As a financial coach, I’ve failed in my job if I offer only upside participation without protecting the downside. But that’s what the average investor experience looks like.

We don’t have to dig far into history to see it. Just rewind five years to the pandemic. The financial desperation then wasn’t limited to the poor; it touched even the average - those who had deemed their jobs steady. And individual adversities are not limited only to mass catastrophes such as the pandemic.

If you want to skip the average pain for good, there’s only one way — have a concrete plan in place.

Everyone Needs a Plan…

The most common excuse — across income levels — for not planning is: “We don’t have enough money to plan with.”

Excuse me? Isn’t that ironic?

If one household has a monthly surplus of ₹10 lakh and another has ₹50,000, who actually needs more discipline in allocating resources?

And what about those who say they have no surplus at all — month after month, year after year? That argument turns even more ironic. Because if you’re not running a surplus, you’re exactly the one who needs to plan better.

Planning is absolutely essential for those trying to break out of the rut. We’ve seen it firsthand. Many of the people we’ve worked with started small and slowly changed the entire trajectory of their financial lives. It gave them not only a concrete optimal path, but also interim milestones for measurable progress to keep them going.

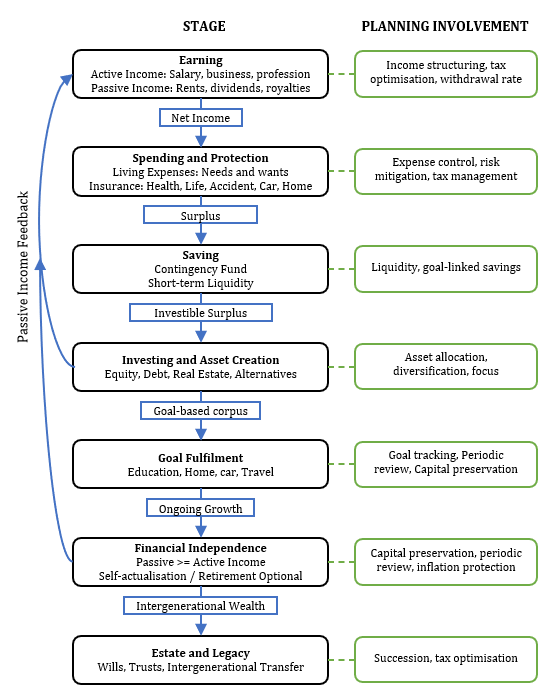

Planning Supports Every Stage of the Financial Lifecycle

And planning isn’t any less valuable for those already wealthy. Many prosperous families became that way by mastering one business or profession — but lasting wealth comes when they diversify across asset classes and geographies, enhance growth while reducing risk, and streamline the passage of wealth to the next generation or towards causes they care about.

…But Most Will Never Have One

I’m not a fan of predictions, but I’ll make one here — this piece won’t move the averages.

Even if I shout from my terrace, urging families to plan and review their finances regularly, the needle will barely move.

The largest distributors and influencers will stay the largest for a long time. Their flywheel is too powerful – it keeps spinning, no matter how they do it – with or without any diligence.

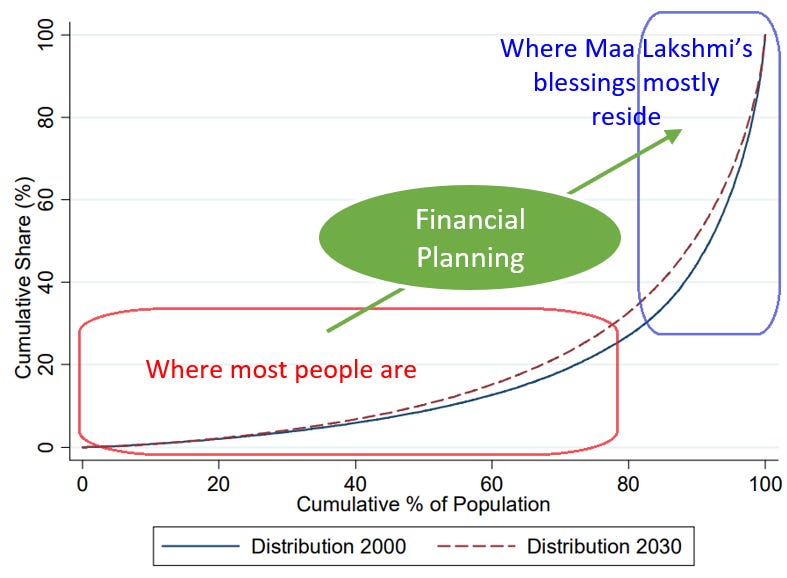

That’s partly why we see an L-shaped wealth distribution in our society — and that shape won’t change just because someone writes a heartfelt blog post.

The Joy of Seeing Plans Work

I may not be able to move the averages much. Still, I feel deeply grateful to have earned the trust of hundreds of individuals across dozens of families — many of you who have stayed with us since the time this work was just a passion project alongside my day job. We have proudly been a partner in your journeys up the L-shaped curve, solidly defying the average experience.

I sleep well knowing you are on solid financial ground. And I’m fairly sure you too sleep better.

It’s now been a year since that passion project became my main body of work. The growing trust and response to my call for planning since then only reinforce one truth — when done right, financial planning changes lives quietly but powerfully.

This Diwali, take it as Maa Lakshmi’s gentle nudge — to take your financial well-being into your own hands, rather than leaving it to unplanned godly luck.

Happy Diwali! 😊

May your wealth be built by design, not by chance.

If reflections like these make money feel a little more human to you, join me at Manchu’s Money Musings — where I try to simplify personal finance, one story at a time.