The Rogue Cannon

The Danger Within

A Fight with a Cannon

It is 1793 – the French Revolution is at its peak. A royalist warship is cutting through the churning waters of the Atlantic. On board are soldiers and officers still loyal to the monarchy, secretly heading to Brittany to ignite rebellion against the new Republican regime.

In the short story that shares its title with this section, Victor Hugo describes a ship built for war—its decks lined with rows of massive black cannons, gleaming and silent like sleeping beasts. These are not merely battle tools, but symbols of power, meant to defend or destroy at a moment’s notice.

Today is one dark, wind-lashed day. The sea is growing wild, and the ship is rolling violently. A cry of despair from the gun-deck startles Captain Boisberthelot. A sudden jolt—a fault in securing the weapons—has sent one of the cannons crashing free. With the ship tilting sharply in the storm, the enormous cannon begins to slide.

What follows is horror.

The 5-tonne cannon, no longer chained, becomes a monster. It roars across the deck with each wave, smashing beams, crushing anything in its path—an iron steamroller turning its own ship into a battlefield. The crew is helpless. Even the bravest sailors have paled at the sight. The side planks, damaged in several places, are beginning to gape open. No enemy can do more damage than this wild machine loose inside the ship’s hull.

One by one, men are being flung aside, chopped like carrots as they try to rein in the metal beast—lest the ship sinks from within.

When Debt Turns Dangerous

Cut to mid-2024. I’m driving back from my relatives’ place in Punjab when I get an urgent call. Someone I know is on the edge — anxious, sleepless, and struggling to survive a couple more months. I have to make a stop en route to my home. There’s no money left. Someone had unmoored the cannon.

We all receive unsolicited calls for, among other things, personal loans, overdraft facilities, credit cards and consumer loans. Many of us, I am sure, do not engage with any of those calls. Till not long before that time, I used to wonder in an age where increasingly smart gadgets are omnipresent, who even listens to these peddlers—let alone buys from them?

But this was the second SOS call I received in six months. In both cases, multiple loans had been taken— personal loans, credit cards, vehicle loans, and loans against their property. In one case, the EMIs were more than double the sole earner’s monthly income. Most of these loans were short-tenured, high-interest, and not used to build assets—just to fund lifestyle expenses.

As with the French warship, the damage was already done. Our only focus now was to moor the cannon again and prevent the ship from sinking.

Healthy Outside, Hurting Inside

A glance at RBI and credit bureau reports offers some backdrop to stories like these.

Post-Covid, household debt in India has grown steadily. It started with out-of-pocket medical costs during the pandemic, then morphed into revenge spending and pent-up consumption.

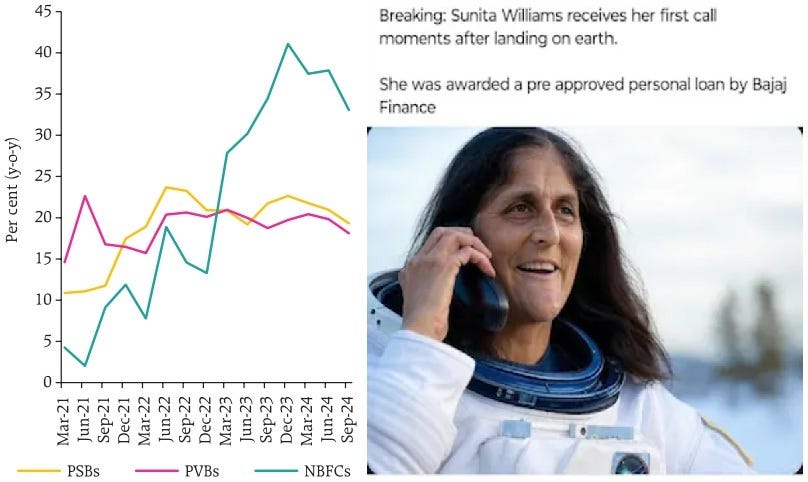

NBFCs have led this debt growth curve, though public and private banks have also grown their portfolios.

Consumer Credit Growth by Lender Type + a painfully relatable meme

The RBI tried to rein in some of the excesses by raising risk weights on certain consumer credit segments in November 2023—including bank credit to NBFCs and unsecured loans (credit cards, personal loans etc.).

Overall, India’s household debt still appears moderate compared to other major economies. So, there is no immediate systemic risk.

On the flip side, some blind spots remain.

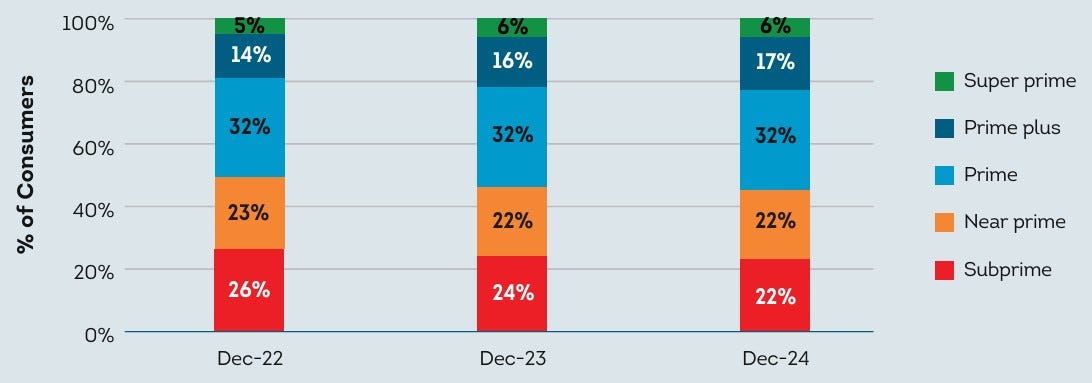

Despite the rise in lending, there hasn’t been a marked increase in 'below-prime' consumers. However, this data doesn’t incorporate debt-to-income ratios. A borrower may have a great credit score but be drowning in EMIs. Such borrowers are not labelled subprime—but perhaps they should be.

Consumer Distribution by Risk Tier

If risk tiers were reclassified using income-debt metrics, I suspect many borrowers would fall from prime to near-prime or subprime. It’s not just one or two outlier ships. Entire fleets are at stake.

Worse, there is no visible data on punitive actions against lenders who knowingly over-lend to people far beyond their repayment capacity. In my view, the absence of proof here is proof of absence.

Furthermore, there’s no data on where this irresponsible lending behavior hurts the most—the grueling years of distress that families endure once they’re overleveraged. This often means facing illegal harassment or drawn-out legal proceedings. Unlike developed economies, where personal bankruptcy is relatively swift, predictable, and free of social stigma, India offers no such relief. As a result, many families, desperate to avoid harassment or litigation, slash their lives to the bare minimum and slog day and night just to stay afloat—maintaining “healthy” credit scores while suffering silently.

In short, the numbers look alright—but they hide more than they reveal.

The Storm Never Ends

Unlike sea winds that blow without intent, spam loan offers are deliberate. They want your cannons to be unmoored.

We know somewhere, some gunner will leave a canon loose. And so do they. We know bankruptcy protections in our country are weak – and so do they. We know unsecured loans won’t get wiped out swiftly upon filing a bankruptcy here – and so do they.

So, no surprise then, when we asked lenders to help with loan consolidation — to lower interest rates, extend tenures and reduce the EMIs — they vanished. These were the same folks who stacked high-interest loans one atop the other a few months ago, even when existing EMIs were already unsustainably high. They will uproot the cannons but never help you moor them back. Their game is profit, and wrecked ships are acceptable collateral.

Even product discounts nudging you toward EMI-based purchases are part of the storm. They shift our perspective to “It’s so affordable” while quietly grabbing large parts of our future income. Think of them as seemingly harmless waves helping the winds loosen the cannon.

Better Safe Than Sunk

So, being eligible for a loan is like bringing a cannon on board. Most of us already have one planted on our ship long ago. We don’t even remember when we were offered our first credit card.

A cannon can protect the ship in adversity — just like loans can be lifesavers in genuine emergencies, especially those you can’t insure against. Rare, but sometimes necessary.

A cannon can also be used to attack — like loans used to fund productive assets. But only when:

The loan is long-term, reasonably priced and not callable at will by the lender

The expected returns clearly outweigh the loan costs

Such situations are rare too.

While the benefits of firing the debt cannon — whether for defense or offence — are rare, what’s far more common is the damage it causes when left unsecured. So, keep the debt cannon solidly moored at all times, and don’t use it for any rogue purpose that’s neither truly defensive nor productively offensive.

Anything potent is equally dangerous when not handled carefully. When your family’s security is at stake, it’s wiser to err on the side of extra caution than to make a seemingly small mistake that could cost you decades of your financial future.

Let’s steer clear of the storms together.

If you know someone already caught in the storm, share this with them. Remind them not to lose heart. Ships can be repaired. Cannons can be chained. It takes time — but recovery is possible, and real.

Being trapped in deep debt is one issue, but a significant portion of society is silently grappling with the reality of being house-rich and cash-poor. Living in a home worth 2 crores yet haggling over a mere 500 bucks with domestic help indicates a severe liquidity crisis. Liquidity has lost its true meaning for many.