In Gold We Trust?

The Golden Soda Can

This is a follow-up to our earlier conversation, In Gold We Trust. Towards the end of that piece, I asked you to forecast gold's returns over the next 5 and 10 years.

Let’s now dive deeper.

The Perfect Metal

There are many rare and shiny metals out there—silver, platinum, palladium. But somehow, gold sits at the top.

Why?

It hits a sweet spot across many important characteristics:

Rare but not too rare: It’s valuable, yet still available enough to be widely used. Unlike rhodium or iridium, which are too scarce for practical monetary systems.

Chemically stable: Doesn’t tarnish, rust, or react easily—unlike silver or osmium.

Malleable & workable: Easy to mould into coins, wires, and jewellery, or other minor industrial applications.

Safe: Non-toxic, biocompatible. You can wear it, store it, and even ingest tiny amounts (e.g. in your chyawanprash).

Store-of-Value Independence from Industrial Volatility: While platinum is tied to cars and palladium to electronics, gold is largely insulated from industrial demand cycles.

Trusted across time: Civilizations have used it for centuries. The trust and liquidity it enjoys are unmatched.

But here’s the twist—none of this makes its price predictable.

Pricing Gold: A Certainly Uncertain Landscape

I chat sometimes with a perennial gold bull. She recently claimed gold could hit ₹3 lakh/10 gm in 5 years— a 3x jump. When asked to back-calculate the annual return, she confidently exclaimed 25% — conservative, she insisted, considering last year’s 30% rise.

But isn’t this a classic case of cherry-picking and extrapolating The Elephant in the Returns?

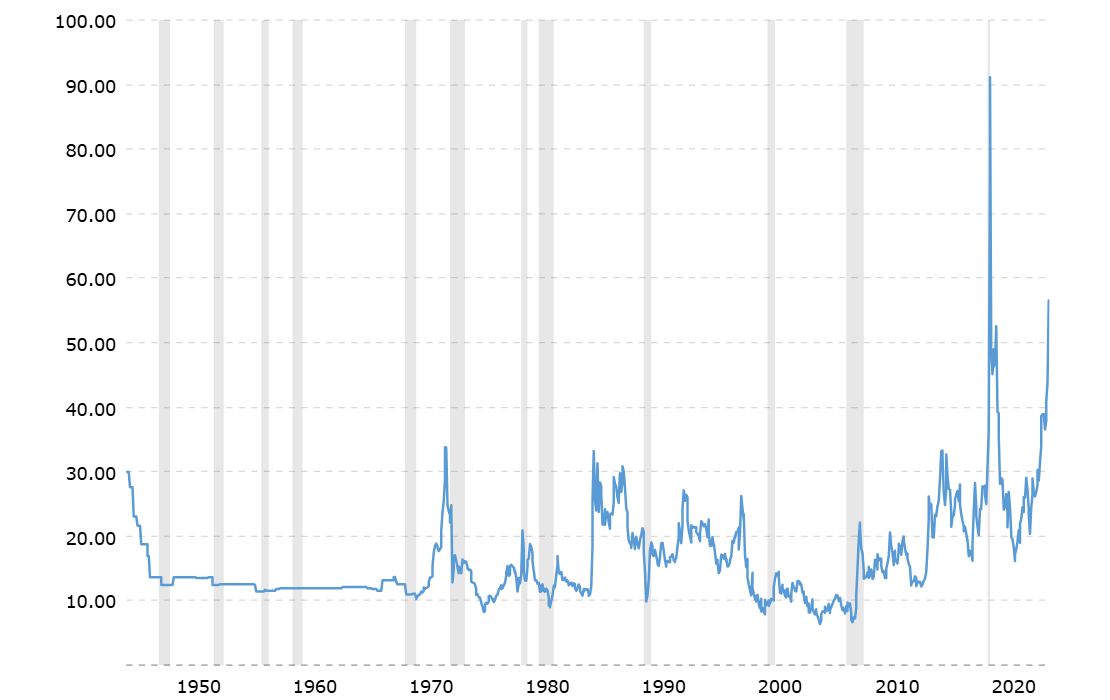

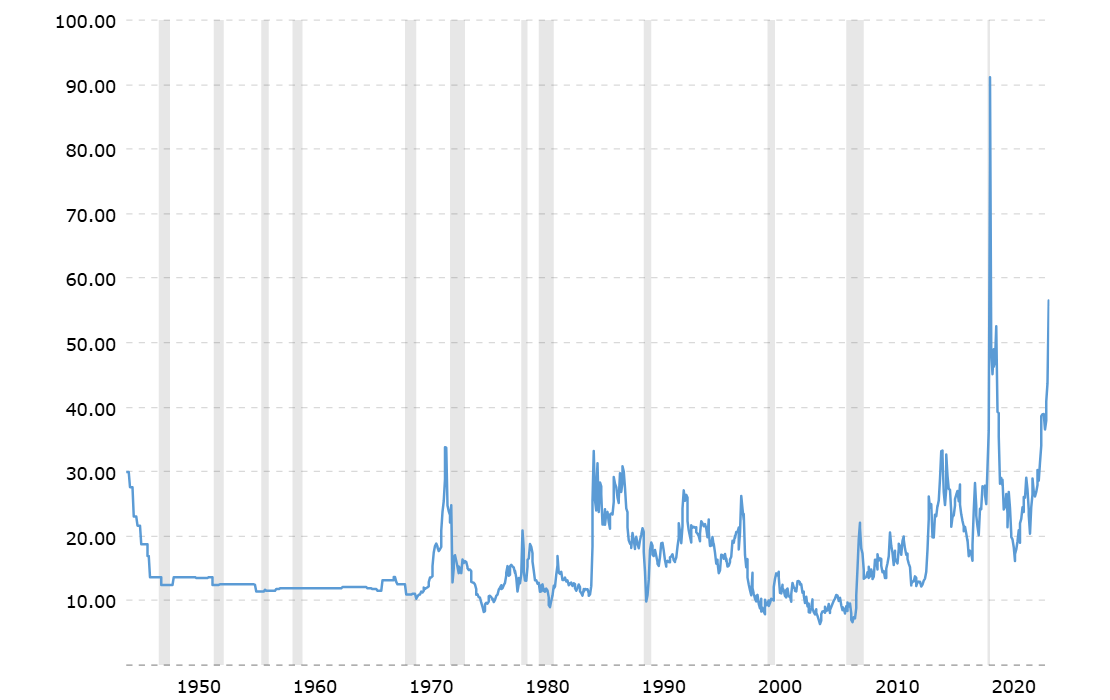

No earnings, no peers, no easy valuation: Gold doesn’t produce anything. No dividends, no interest, no cash flows. The often-quoted gold-to-oil ratio offers a vague reference point. Going by that, the metal currently looks overvalued.

Source: Macrotrends So, a mean reversion of this ratio could imply pain ahead for gold prices.

The Noble Downgrade: Napoleon III—President and later Emperor of France from 1848 to 1870—modernised the economy, beautified Paris, expanded the empire, and built the world’s second-largest merchant navy.

Naturally, his most honoured guests were served using the finest cutlery—crafted not from gold, but from aluminium. Yes, the same grey stuff in today’s frying pans and soda cans!

But aluminium wasn’t ordinary then. It was rarer and costlier than gold. In 1884, a 3-kg aluminium cap placed atop the Washington Monument was hailed as a “marvel of science and wealth.” At the time, it was the largest piece of aluminium ever cast. Aluminium was rare because it was difficult to extract economically in large quantities.

Then came the Hall-Héroult process in 1886. Aluminium suddenly became easy and cheap to produce. What was once elite became ordinary.

Could the same happen to gold?

New, large-scale discoveries can have outsized impacts.

Deep-sea and asteroid mining are no longer science fiction. Real companies are actively pursuing permits and developing technology to commence operations.

While the likelihood seems low at present, if gold were to lose its scarcity, its premium pricing would vanish as well. Imagine sipping from golden soda cans or eating from a golden lunchbox!

This is why, over longer horizons, I see risk of a massive crash, let alone consistent returns matching or beating inflation.

Did your 5- or 10-year return forecasts (from last week) factor in these potential game-changers?

The Hidden Costs: Security & Standardisation

Gold is a magnet for crime—snatching, robbery, fraud and theft.

Haircuts on resale: Selling physical gold often means deductions for impurities, making charges, and poor standardisation—even with bars. Hallmarking helps, but the risks remain.

So, What Are We Really Holding?

Tying last week’s post with today’s reflections:

Gold may look like insurance—but for a retail investor, it doesn’t insure much.

It doesn’t behave like a good investment.

There’s no robust basis to forecast its price.

Even if you buy ratios like gold-to-oil, there’s a case for near-term downside.

There’s a small (and increasing) chance of major value destruction in the long term if scarcity disappears.

Security risks make physical gold even less attractive.

It can be a good refuge: One sensible reason to ‘invest’ in gold seems to be in extreme scenarios— think prolonged civil unrest, war, tyrannical rule, or a collapsing economy. In such cases, escaping with your wealth in a compact, globally accepted form becomes crucial. But this doesn’t sound like India right now.

Also, let’s not ignore one reason that drives gold demand in India: To stash ‘that’ cash.

So yes, there are reasons people buy gold.

But that doesn’t make it an investment—it makes it a refuge, or a workaround.

Shrink your Golden Goose?

Some commentators say sustained central bank buying hints at deeper, structural changes. There is something more than meets the eye, they argue. Couple of thoughts on this:

Even after heavy central bank buying, gold is still only ~11% of India’s forex reserves and ~5% of China’s.

Perhaps something is missing in our analysis. Perhaps you should give 5–10% of your invested assets to gold, as some apparently balanced voices suggest. (Of course, avoid the apocalyptic narratives often attached to gold by its most fervent advocates)

Go ahead. Do it please.

The conundrum is – To reach even 10% of invested assets, many Indian families will need to sell some of their beloved gold holdings. And the high price environment provides a wonderful exit window for this.

This is the more pressing structural change that is long overdue on many personal portfolios, imho. Will you do this rebalancing? 😊

If not, just know that your gold is tradition, culture, aesthetic indulgence, refuge, or speculation—but not an investment or insurance.

If you enjoyed this, scroll down a bit more and hit that heart — it’ll make my day!

And if you think a friend might enjoy it too, go ahead and share it.